")

")

Balanced Scorecard (BSC) approach: definition, limits and benefits

1. Background of the Balanced Scorecard approach

Created in the 1990s by professors Robert Kaplan and David Norton, the Balanced Scorecard approach was conceived as a response to the limitations of traditional approaches to performance measurement, which focused almost exclusively on financial indicators. These approaches, while important for assessing profitability and financial stability, often ignored other essential aspects of business performance such as customer satisfaction, the efficiency of internal processes and the ability to innovate and adapt to change.By providing a framework for measuring these otherwise neglected aspects of performance, BSC has brought a new balance to performance measurement, enabling companies to better align their activities with their overall strategy and achieve sustainable performance over the long term.

2. Key principle of the Balanced Scorecard: Balance

The central principle of the Balanced Scorecard is balance. In other words, it encourages organisations not to focus solely on a single measure of performance, but to balance a range of different measures that reflect all the important dimensions of performance. This principle of balance is manifested through the four BSC perspectives, which together provide a comprehensive and balanced view of business performance.3. Popularity of the Balanced Scorecard

Since its inception, the Balanced Scorecard has been widely adopted by organisations of all types and sizes. According to a Bain & Company study cited by Forbes in 2014, around half of companies worldwide use the BSC or a similar approach to measure their performance and align their strategic objectives. In Bain & Company's "Management Tools & Trends" study (2015), BSC was among the 25 most widely used management tools in the world.4. Structure of the Balanced Scorecard : examples

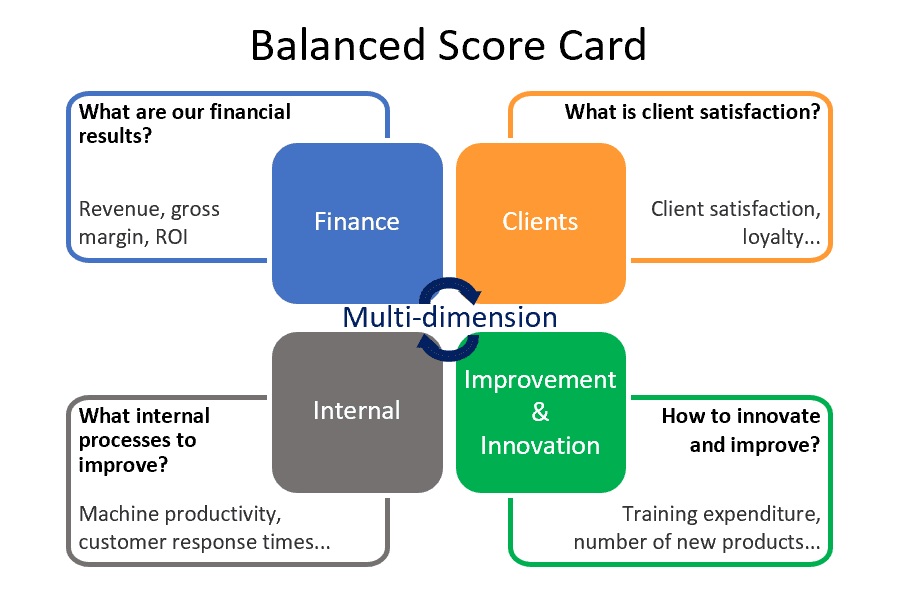

The Balanced Scorecard is made up of four perspectives: financial, customer, internal processes, and learning and growth.- Financial perspective: The objectives of this perspective are often linked to financial results such as profitability, revenues and return on investment. How is the company perceived by its shareholders and what are its financial results?

- Examples of KPIs: revenue, gross margin, return on investment (ROI), cost of customer acquisition.

- Customer perspective: This perspective focuses on how the organisation is perceived by its customers, with indicators such as the customer satisfaction rate and the customer loyalty rate. How is the company perceived by its customers and what are its objectives in terms of customer satisfaction?

- Examples of KPIs: customer satisfaction rate, customer loyalty rate, conversion rate from prospects to customers.

- Internal Process Perspective: The objectives of this perspective relate to the effectiveness and efficiency of the organisation's internal processes, such as production cycle time and defect rate. Which internal processes need to be improved in order to achieve the company's objectives?

- Examples of KPIs: production cycle time, percentage of defective products, response time to customer service requests.

- Learning and Growth Perspective: This perspective focuses on the organisation's ability to innovate and learn, with indicators such as training expenditure per employee and the number of new products launched. How can the company improve, innovate and create value in the future?

- Examples of KPIs: training expenditure per employee, percentage of employees undergoing training each year, number of new products or services launched each year.

For more information on choosing KPIs, you can consult our views on the SMART methodology at How many KPIs do we need? or on leading and lagging indicators.

5. Benefits and limitations of the Balanced Scorecard Balanced Scorecard

There are three main benefits of the Balanced Scorecard approach:- A global view of the company's performance: The BSC enables companies to track a wide range of performance indicators, not just financial measures. This gives a more complete picture of the health and performance of the business.

- Strategic alignment: BSC helps to align the company's objectives and initiatives with its overall vision and strategy.

- Communication and understanding: BSC makes it easier for all staff to communicate and understand the company's strategy.

Risks or limitations of the Balanced Scorecard:

- Complexity: Setting up and managing a BSC can be complex and require a lot of time and resources. This can be particularly difficult for small businesses.

- Choice of indicators: Choosing the right performance indicators can be a challenge. Poorly chosen indicators can give a distorted picture of the company's performance.

- Overweighting of quantitative measures: Although BSC encourages the use of a variety of performance indicators, it can still favour quantitative measures over qualitative ones.

6. The Balanced Scorecard approach and other management methodologies

The Balanced Scorecard approach complements other management methodologies such as Management by Objectives (MBO), Objectives and Key Results (OKR), and the SMART methodology. For example, the objectives set as part of the BSC can be defined in SMART (Specific, Measurable, Achievable, Relevant and Time-bound) terms to ensure they are clear and achievable. Similarly, BSC and MBO share a common focus on the alignment of individual and organisational objectives.7. Conclusion

The Balanced Scorecard approach s a powerful tool for balancing performance indicators and aligning an organisation's activities with its vision and strategy. Although it has its limitations, its widespread adoption and its ability to complement other management approaches attest to its value as a performance measurement framework.Stay Informed

When you subscribe to the blog, we will send you an e-mail when there are new updates on the site so you wouldn't miss them.

Comments